Booming Nigerian Fintech Sector Could See Revenues Reach US$543M by 2022

by Fintechnews Africa 7 December 2020Fintech revenues in Nigeria are projected to reach an estimated US$543 million by 2022, driven by increasing smartphone penetration and a large population of unbanked eager to adopt digital financial services, according to a new report by the Economist Intelligence Unit (EIU).

The report, titled State of Play: Fintech in Nigeria, examines key trends in the Nigerian fintech sector, and assesses industry drivers.

According to the study, Nigeria is home to a burgeoning fintech startup community and is rapidly emerging as one of Africa’s fintech leaders. McKinsey estimates that there are currently over 200 fintech standalone companies in the country, in addition to fintech solutions offered by banks and mobile network operators as part of their product portfolio.

These players are attracting the attention of international investors who are now pouring millions into the country’s most promising startups. Between 2014 and 2019, fintech companies in Nigeria raised over US$600 million in funding with the most of that amount (US$460 million) being raised in 2019 alone. This showcases that much of the industry’s growth has happened over the past year or so. Deals included Migo’s US$20 million Series B, Paga’s US$10 million funding round and Lidya’s US$6.9 million Series A.

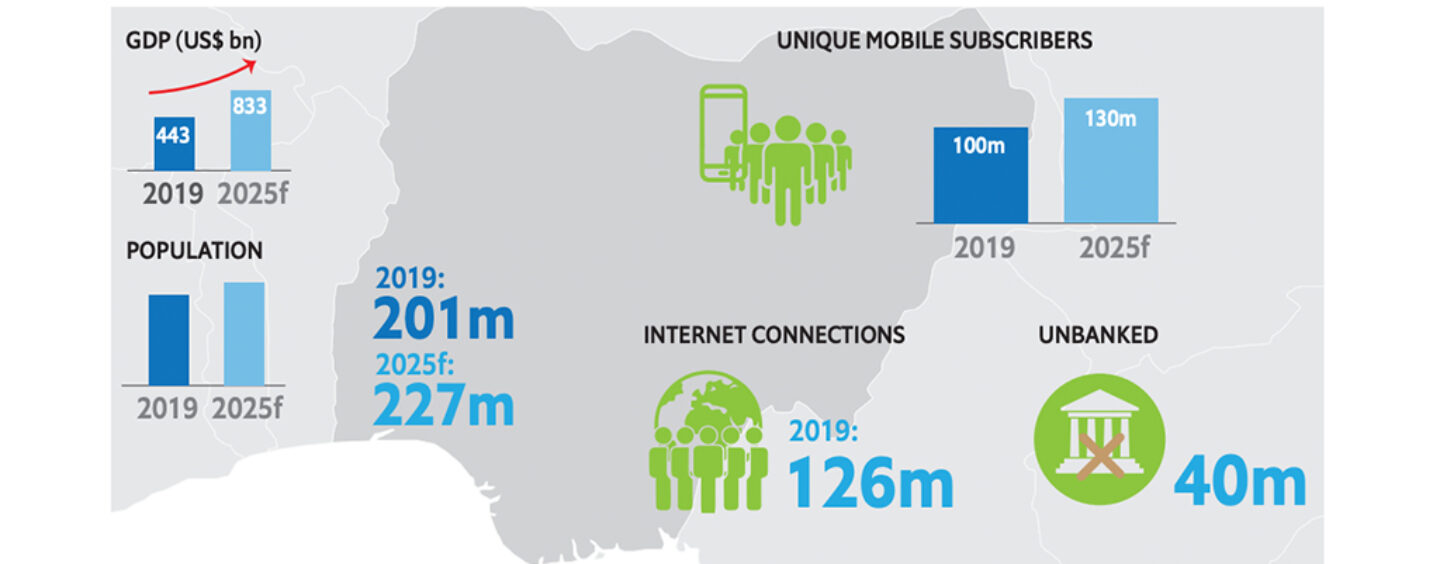

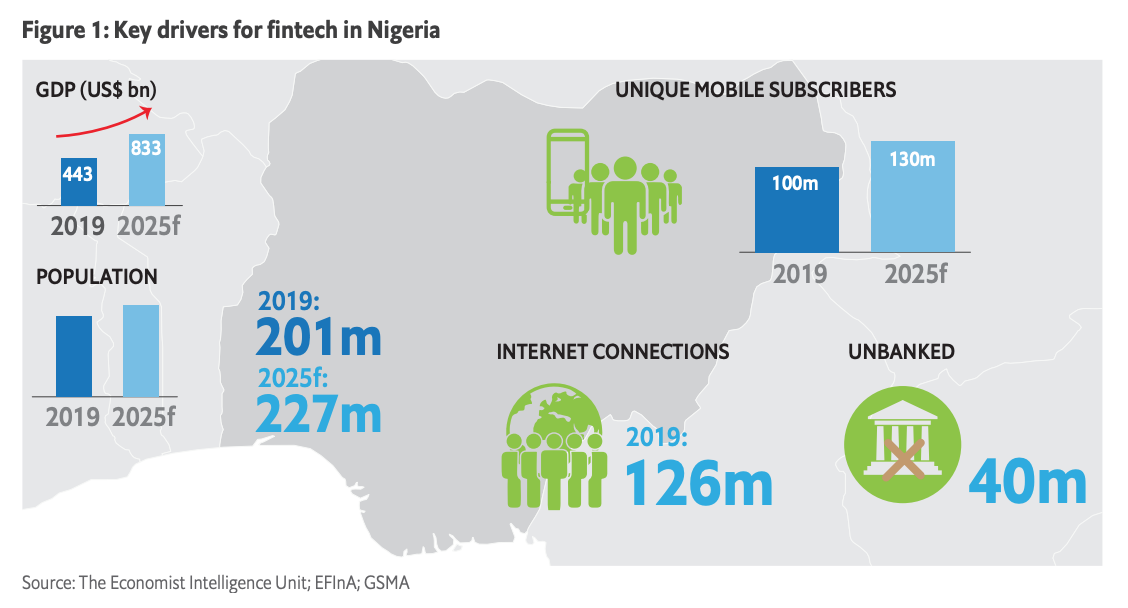

Fintech in Nigeria: industry drivers

Nigeria is home to Africa’s largest economy and a population of more than 200 million, among which about 40% being financially excluded. This, combined with rising Internet and smartphone penetration, is offering plenty of opportunities for tech startups to develop and provide the community for affordable and convenient digital financial services.

Key drivers for fintech in Nigeria, Source: State of Play: Fintech in Nigeria, Economist Intelligence Unit (EIU), June 2020

A McKinsey report released in September 2020 notes several areas in particular where fintechs could make a difference. In consumer finance, both young and senior affluent individuals still face poor user experience, giving fintechs the opportunity to offer seamless, digital-first products and value-added services.

Small and medium-sized enterprises (SMEs) also face numerous challenges, including limited access to financing. PwC Nigeria estimates that the yearly financial gap for Nigerian micro, small and medium-sized enterprises (MSMEs) is at an astonishing NGN 617.3 billion (US$1.6 billion).

Nigeria’s fintechs

Similarly to other markets, fintech activity in Nigeria started with payments before expanding into other areas. To this day, payments and remittances still remain the most developed fintech segment in Nigeria with providers that include Paga, OPay, Cellulant, Interswitch’s QuickTeller, as well as Chipper Cash.

But most recently, activity began picking up strongly in lending, with a surge in mobile products targeting SMEs and retail sectors, the EIU report notes. Startups like Carbon, formerly Paylater, and Renmoney, are leveraging alternative credit-scoring algorithms to provide instant, unsecured, short-term loans to individuals, while others, like Migo, are offering unsecured working-capital loans to SMEs with minimal documentation.

Wealthtech and savings are other hot segments. Services including CowryWise and PiggyVest are bringing online savings and investment products to the country’s millennials and young professionals. Bankly is a savings app focused on the informal mass market, and Farm Crowdy provides investors with investment opportunities in Nigeria’s agricultural sector. Fintechs operating in asset management are also multiplying in number with companies like RiseVest, Chaka and Bamboo offering users the possibility to invest in international stock markets.

Insurtech is another emerging fintech segment in Nigeria, which has seen the entrance of players like Cassava Smartech, a provider of auto, education and health coverage with prices as low as US$0.5 a month, and AutoGenius, an online insurance comparison platform.

Non-cash transaction volume is forecast to grow at a compound annual growth rate (CAGR) of 39% between 2018 and 2023, according to a report by Nigerian financial resource company Nairametrics. Non-cash transactions are expected to represent 17.8% of all transaction volume by 2023, rising from just 4.7% as of the end of 2018.

This article first appeared on fintechnews.ae.

{kind=link}

2 Comments so far

Jump into a conversation